SUMMARY:

SUMMARY:

60 – 70 years ago, natural gas was an unpopular commodity unearthed when searching oil. The saying: “Find gas once and you will be forgiven, twice and you will be fired.” was well known in the oil industry. Consequently, it is no exaggeration to say that natural gas pricing has always interacted with the prices of substitutes. Historically in the US natural gas market “cost plus” pricing that is similar to oil production and in the European perspective oil-indexed pricing has been popular before. So how will this pricing evolve in to the future?

METHOD:

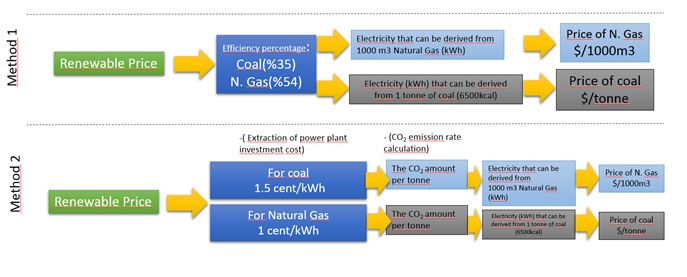

A method based on determining electricity amount that can be gained from a unit of coal and natural gas priced on the recent renewable prices is calculated. All heat units were converted to kWh as common energy units. For example, kWh in 1000m3 natural gas, kWh in 1 ton coal (6500kcal) was determined. These quantities of energy were multiplied by the electricity conversion efficiencies to find the amount of electricity that could be obtained from 1 ton of coal and 1000 m3 of natural gas. Then this electricity kWhs to be obtained from unit fossil fuels are multiplied by renewable prices. This provides us the same services based on same kWh set by renewable prices.

In general, electricity generated by renewables and electricity generated by fossil fuels may not be the “same bundled electricity services”. That is to say, the fossil fuel power plants can provide load following or can respond to load fluctuations. However renewable kWhs themselves change instantaneously and can not provide load following.

Carbon pricing is important in terms of understanding developments in the UK and Europe. It is possible to make one source less economical than the other by mandating a carbon price. Similarly, France’s carbon price proposal sheds light on reasoning behind Germany’s decision to remain away for now to protect lignite reserves. Neverthless, carbon price can also be representative as the price tag for the burden of burning such fuel.

IF RENEWABLE PRICES SET FOSSIL FUEL PRICES:

Although hub-based, index-based pricing will be an important part of the future market structure, the fact that competition and elasticities between fuels will be the determinant of economic rules and consumption. Price level itself is not the major factor, but price level relative to substitutes is more important.

The table below has 4 main columns. In the first twin columns renewable prices has been assumed as electricity prices to be gained from a unit of fossil fuel. For the second column, renewable prices have been equated to fossil fuel costs plus capital investment costs. In renewables the kWh price is the price of everything since no fuels are burned. Thus, fossil fuel costs will have to be lower. (Such as, if electricity sells for 4 cents and pays the capex costs with 1 cent/kWh, the remaining 3 cents/kWh is for the fuel cost)

The third and fourth columns are important to understand how each $10 carbon price changes the prices.

| Without investment costs | Without emission pricing | 10$/tonnes CO2 emission pricing | 20$/tonnes CO2 emission pricing | |||||

| Renewable

(c/kWh) |

Natural Gas

($/1000m3) |

Coal

($/tonne) |

Natural Gas | Coal | Natural Gas | Coal | Natural Gas | Coal |

| 4 | 230 | 105 | 172 | 66 | 151 | 37 | 130 | 8 |

| 3,5 | 201 | 92 | 144 | 52 | 122 | 24 | 101 | -5 |

| 3 | 172 | 79 | 115 | 39 | 94 | 11 | 72 | -18 |

| 2,5 | 144 | 66 | 86 | 26 | 65 | -2 | 44 | -31 |

| 2 | 115 | 52 | 57 | 13 | 36 | -15 | 15 | -44 |

RESULTS:

If we assume that natural gas was priced relative to oil in the 20th century, the question of how natural gas will be priced in the 21st century, when oil demand is under doubt, will be a million dollar question. For traders it is the hub, the stock market, the index. From the final consumption’s perspective, the price we pay for new resources to get the same services we obtain from fossil fuels will decisive.