SUMMARY

SUMMARY

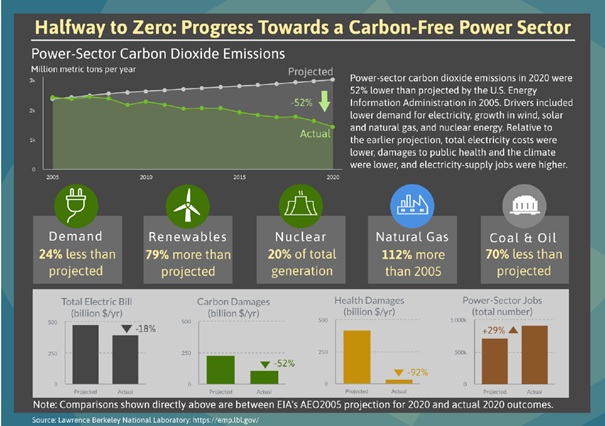

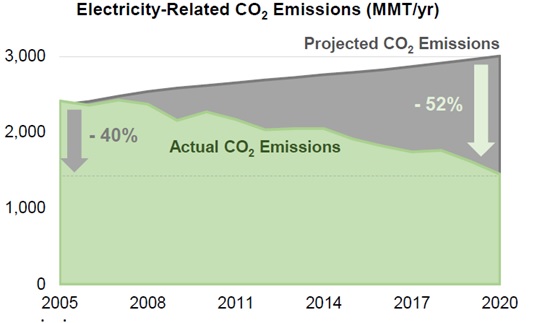

Sharply reducing carbon emissions is imperative to prevent the worst effects of climate change. Fifteen years ago, many business-as-usual projections anticipated that annual carbon dioxide (CO2) emissions from power supply in the United States would reach 3,000 million metric tons (MMT) in 2020. In fact, direct power-sector CO2 emissions in 2020 were 1,450 MMT—roughly 50% below the earlier projections. By this metric, in only 15 years the country’s power sector has gone halfway to zero emissions. Other metrics also evolved differently than projected: total consumer electricity costs (i.e., bills) were 18% lower; costs to human health and the climate were 92% and 52% lower, respectively; and the number of jobs in electricity generation was 29% higher. Economic, technical, and policy factors contributed to this success, including sectoral changes, energy efficiency, wind and solar, continued operations of the nuclear fleet, and coal-to-gas fuel switching.

This historical record demonstrates the ability of technological and policy changes to set the power sector on a dramatically different emissions trajectory. Past success, however, does not trivialize the challenges that remain for further decarbonization in the power sector and beyond. Nor does it offer a specific roadmap for how best to achieve additional power-sector emissions reductions Numerous challenges confront a zero-emissions pathway, and future strategies will likely differ from those of the past. Many recent studies have assessed how to make further progress in decarbonizing the power sector on the pathway to decarbonizing the economy as a whole, including a report from the NationalAcademies (2021a). As the country maps out a plan for further decarbonization, experience from the past 15 years offers two central lessons. First, policy and technology advancement are imperative to achieving significant emissions reductions. Second, our ability to predict the future is limited, and so it will be crucial to adapt as we gain policy experience and as technologies advance in unexpected ways.

Key findings on emissions reductions to date

Lower Emissions: The U.S. power sector, in 2020, looks radically different from projections made 15 years earlier. Compared to a range of past business-as-usual projections from the government, private sector, and research communities, in just 15 years the country’s power sector has marched halfway to zero emissions. For example, the U.S. Energy Information Administration’s (EIA’s) 2005 Annual Energy Outlook (AEO) projected that CO2 emissions from power supply would be 3,008 MMT in 2020. In fact, direct power-sector CO2 emissions in 2020 were 1,450 MMT, 52% lower than projected. The results for 2020 reflect the impact of COVID-19. Electricity demand in 2020 was 4% lower than in 2019. The 52% reduction in emissions relative to EIA’s earlier business-as-usual projection is reduced to 46% if 2019 data are used. Comparing 2020 power-sector CO2 emissions with 2005 emissions shows a more modest though still sizable 40% reduction. Using pre-COVID data from 2019, the reduction is 33%—on this latter metric, the United

States is one third of the way towards zero emissions.

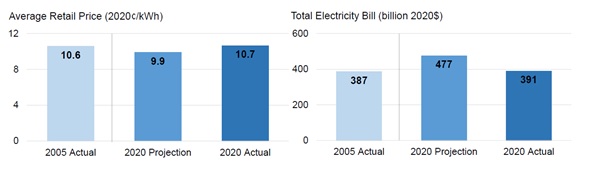

Limited National Consumer Electricity-Cost Impacts: Retail electricity prices in 2020 (10.7 cents per kilowatt-hour [¢/kWh]) were similar to those in 2005 (10.6 ¢/kWh, in real 2020$), but higher than projected for 2020 (9.9 ¢/kWh). Total sales in 2020 were lower than anticipated. Consequently, total customer electricity bills (i.e., costs) in 2005 and 2020 were similar, and 2020 bills—at $391 billion—were 18% lower than the projected $477 billion. However, they indicate that national average electricity expenditures are roughly the same today as in 2005, and they are well below previously projected values.

Lower Health and Climate Burdens: The impacts of electricity supply go well beyond consumer electricity bills to include climate damages caused by carbon emissions and human health damages from other pollutants. Climate damages from power-sector carbon emissions in 2020, estimated at $110 billion, were less than half the $229 billion that would have been incurred under the EIA projection. In total, the calculated social cost of power supply—considering electricity bills, climate damages, and health impacts—in 2020 of $535 billion was 44% lower than in 2005 ($948 billion) and 52% lower than projected for 2020 ($1,124 billion).

National Power-Supply Job Gains: Electricity-supply related employment in 2019 (the most recent year for which comprehensive data are available) was 29% higher than might have been the case under the business-as-usual projection for 2020, because the renewable energy sector is job-intensive, requiring more jobs per unit output than natural gas and coal. As a result, though jobs in the coal sector are considerably lower than might have been the case, natural gas and especially renewable energy jobs boost the overall total to 920,000. Jobs in the nuclear sector largely held steady.

Slower Progress in Other Energy Sectors: Decarbonization in other energy sectors has been slower than in the power sector, which accounts for 53% of total energy-sector emissions reductions. Nonetheless, trends since 2005 and comparisons to projections for 2020 show broad progress. Total energy-related carbon emissions in 2020 were 39% lower than projected under the EIA’s business-as-usual scenario.

Future pathways and remaining challenges

It is significant that the nation has cut power-sector carbon emissions over the last 15 years. However, if the United States is to progress on a deep-decarbonization pathway, it must absorb the likely near-term rebound in emissions post-COVID, and then once again beat business-as-usual emissions projections. Many challenges confront a zero-emissions pathway, and the strategies of the future will differ from those of the past. Recent literature suggests the following future pathways and challenges:

Deep Additional Reductions at Relatively Low Incremental Cost: Recent literature suggests that solar, wind, and energy storage—along with existing low-carbon resources and energy efficiency—are likely to play important roles in near-term power-sector decarbonization. Given advancements in wind, solar, and battery technologies, decarbonizing the power sector now appears to be more cost-effective than expected just a few years ago. Moreover, more than half of the additional wind and solar capacity needed to approach a zero-carbon power-sector target is already in the development pipeline: about 660 gigawatts (GW) of wind and solar are seeking transmission access (along with about 200 GW of storage).

Challenges Ahead in Scaling Wind, Solar, and Storage: Dramatically expanding wind, solar, and storage to become major contributors to power supply is not trivial. It would require extensive efforts to ensure electricity delivery and power-system reliability and resilience, significant new transmission infrastructure, enhanced and integrated planning and operations, revised siting processes, focused attention on workforce and supply chain issues, and heightened responsiveness to impacted communities. Aggressive pursuit of energy efficiency and demand response—in part through grid-interactive efficient buildings—can address some of these challenges, but it may create new challenges in system coordination given the increasingly complicated operating environment.

Striving for Zero Emissions: For power systems relying on increasing volumes of wind, solar, and batteries, the incremental cost of carbon reduction begins to rise more steeply as emissions decline and eventually approach zero. Further research, development, and demonstration for the numerous technologies that can fill this gap in the puzzle is needed, to enable technology portfolios that minimize incremental costs. Options include longer-duration storage, hydrogen or synthetic fuels, biofuels, fossil or biomass with carbon capture, nuclear, geothermal, and solar-thermal with storage.

Moving Beyond the Power Sector: The power sector is widely viewed as a cornerstone for economy-wide decarbonization, through electrification of other energy end uses. Of course, electrification alone will not yield a zero-carbon economy; many applications cannot be electrified at reasonable cost, given current technology. These additional emissions sources are sizable and may prove more challenging to decarbonize, requiring a different set of technologies and policies.

Source: “Halfway to Zero: Progress towards a Carbon-Free Power Sector”, Berkeley Lab