SUMMARY

SUMMARY

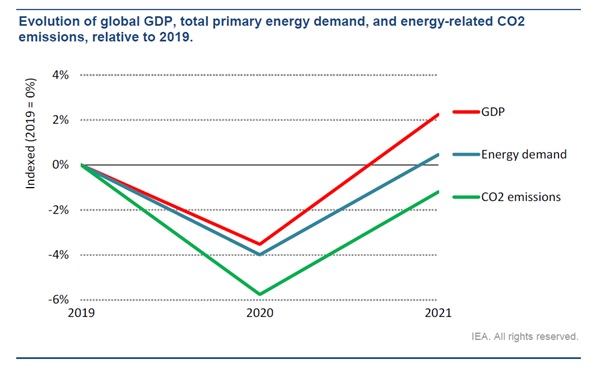

Global energy demand in 2020 fell by 4%, the largest decline since World War II and the largest ever absolute decline. The latest statistical data for energy demand in the first quarter of 2021 highlights the continued impacts of the pandemic on global energy use. Building on Q1 data, projections for 2021 indicate that as Covid restrictions are lifted and economies recover, energy demand is expected to rebound by 4.6%, pushing global energy use in 2021 0.5% above pre-Covid-19 levels. The outlook for 2021 is, however, subject to major uncertainty. It depends on vaccine rollouts, the extent to which the Covid-19-induced lockdowns scarred economies, and the size and effectiveness of stimulus packages. Current economic outlooks assume global GDP will surpass 2019 levels, lifting demand for goods, services and energy. However, transport activity and, particularly, international travel remain severely supressed. If transport demand returns to pre-Covid levels across 2021, global energy demand will rise even higher, to almost 2% above 2019 levels, an increase broadly in line with the rebound in global economic activity.

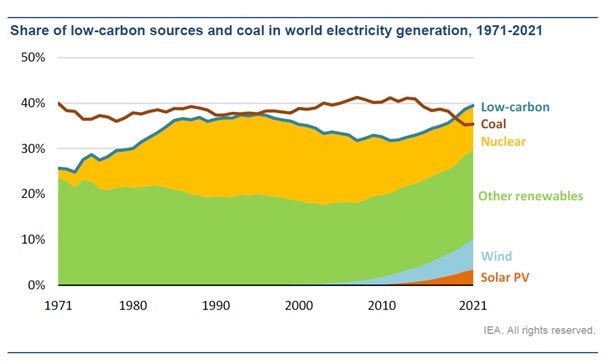

Increases in electricity generation from all renewable sources should push the share of renewables in the electricity generation mix to an all-time high of 30% in 2021. Combined with nuclear, low-carbon sources of generation well and truly exceed output from the world’s coal plants in 2021.

Key findings in the report are as follows:

- The Covid-19 pandemic continues to impact global energy demand. Third waves of the pandemic are prolonging restrictions on movement and continue to subdue global energy demand. But stimulus packages and vaccine rollouts provide a beacon of hope. Global economic output is expected to rebound by 6% in 2021, pushing the global GDP more than 2% higher than 2019 levels

- Emerging markets are driving energy demand back above 2019 levels. Global energy demand is set to increase by 4.6% in 2021, more than offsetting the 4% contraction in 2020 and pushing demand 0.5% above 2019 levels. Almost 70% of the projected increase in global energy demand is in emerging markets and developing economies, where demand is set to rise to 3.4% above 2019 levels. Energy use in advanced economies is on course to be 3% below pre-Covid levels.

- Global energy-related CO2 emissions are heading for their second-largest annual increase ever. Demand for all fossil fuels is set to grow significantly in 2021. Coal demand alone is projected to increase by 60% more than all renewables combined, underpinning a rise in emissions of almost 5%, or 1 500 Mt. This expected increase would reverse 80% of the drop in 2020, with emissions ending up just 1.2% (or 400 Mt) below 2019 emissions levels.

- Sluggish demand for transport oil is mitigating the rebound in emissions. Despite an expected annual increase of 6.2% in 2021, global oil demand is set to remain around 3% below 2019 levels. Oil use for road transport is not projected to reach pre-Covid levels until the end of 2021. Oil use for aviation is projected to remain 20% below 2019 levels even in December 2021, with annual demand more than 30% lower than in 2019. A full return to pre-crisis oil demand levels would have pushed up CO2 emissions a further 1.5%, putting them well above 2019 levels.

- Global coal demand in 2021 is set to exceed 2019 levels and approach its 2014 peak. Coal demand is on course to rise 4.5% in 2021, with more than 80% of the growth concentrated in Asia. China alone is projected to account for over 50% of global growth. Coal demand in the United States and the European Union is also rebounding, but is still set to remain well below pre-crisis levels. The power sector accounted for only 50% of the drop in coal-related emissions in 2020. But the rapid increase in coal-fired generation in Asia means the power sector is expected to account for 80% of the rebound in 2021.

- Among fossil fuels, natural gas is on course for the biggest rise relative to 2019 levels. Natural gas demand is set to grow by 3.2% in 2021, propelled by increasing demand in Asia, the Middle East and the Russian Federation (“Russia”). This is expected to put global demand more than 1% above 2019 levels. In the United States – the world’s largest natural gas market – the annual increase in demand is set to amount to less than 20% of the 20 bcm decline in 2020, squeezed by the continued growth of renewables and rising natural gas prices. Nearly three-quarters of the global demand growth in 2021 is from the industry and buildings sectors, while electricity generation from natural gas remains below 2019 levels.

- Electricity demand is heading for its fastest growth in more than 10 years. Electricity demand is due to increase by 4.5% in 2021, or over 1 000 TWh. This is almost five times greater than the decline in 2020, cementing electricity’s share in final energy demand above 20%. Almost 80% of the projected increase in demand in 2021 is in emerging market and developing economies, with the People’s Republic China (“China”) alone accounting for half of global growth. Demand in advanced economies remains below 2019 levels.

- Renewables remain the success story of the Covid-19 era. Demand for renewables grew by 3% in 2020 and is set to increase across all key sectors – power, heating, industry and transport – in 2021. The power sector leads the way, with its demand for renewables on course to expand by more than 8%, to reach 8 300 TWh, the largest year-on-year growth on record in absolute terms.

- Renewables are set to provide more than half of the increase in global electricity supply in 2021. Solar PV and wind are expected to contribute twothirds of renewables’ growth. The share of renewables in electricity generation is projected to increase to almost 30% in 2021, their highest share since the beginning of the Industrial Revolution and up from less than 27% in 2019. Wind is on track to record the largest increase in renewable generation, growing by 275 TWh, or around 17%, from 2020. Solar PV electricity generation is expected to rise by 145 TWh, or almost 18%, and to approach 1 000 TWh in 2021.

- China alone is likely to account for almost half the global increase in renewable electricity generation. It is followed by the United States, the European Union and India. China is expected to generate over 900 TWh from solar PV and wind in 2021, the European Union around 580 TWh, and the United States 550 TWh. Together, they represent almost three-quarters of global solar PV and wind output.

Source: “Global Energy Review 2021”, IEA